These Horizon Notebooks present our intuitions, strategic reflections, and fundamental questions. We return to a core subject and take a step back from the daily grind. This is an opportunity for us to look ahead and focus for a moment on the compass that guides us. This report explores the concept of territorial finance. Between system analyses, legacies from the past, and operational challenges, this notebook explores the benefits of a financial system reconnected to the limits of our ecosystems and the needs of communities, both present and future. Enjoy the read! 😊

The Social and Solidarity Economy (ESS) sector in France is in crisis. The decline in public subsidies is undermining an entire sector of the economy that still serves as a bulwark against the excesses of capitalism. ESS actors now find themselves having to choose between reducing their activities (not renewing positions and layoffs), hybridizing their activities (often by entering into competition on service activities), or accepting financing conditions that are barely sustainable for teams (certain structural costs no longer being covered, increasing complexity of budgetary arrangements, etc.).

Explaining this evolution as simple "political choices" at the national level would cause us to miss more structural reasons. These choices are themselves part of a more complex macro context (geopolitical tensions, wealth concentration, questioning of multilateralism, etc.) whose effects trickle down in cascades to our territories.

Faced with these observations, two choices are possible: resign and adapt to a context that seems beyond us; or identify the levers that we can still activate at our scale. This notebook adopts the second stance. Among these structural issues, finance seems to us to be one of the levers on which we have the capacity to act and experiment locally.

In this notebook, we will strive to answer three questions:

- How does the financial system impact our territories and our structures?

- How would the relocalization of finance allow us to rethink the rules of the game?

- How can we translate an ideal and long-term vision into an operational project capable of meeting immediate needs on the ground?

1/ The four drifts of global finance

Finance can be perceived as the nervous system of our "society" super-organism. This system is remarkably powerful: it connects 8 billion people who cooperate to run the supply chains, institutions, and local services that allow us to live together. But without a collective awareness of this power, we use this tool to serve our short-term needs without visibility or understanding of the slippery slope upon which we are walking.

This slope can be characterized by 4 principles structurally embedded in the financial system, which is currently: (i) a generator of instability for the economy; (ii) a source of growing inequalities; (iii) a destroyer of natural resources; and (iv) unjust toward future generations.

1. A monetary and financial system inherently unstable #instability

The current financial system functions like an engine in a state of permanent overheating. Designed to promote the rapid circulation of flows, it has become intrinsically unpredictable and subject to systemic shocks that exceed local regulatory capacities. This instability is not the result of random accidents, but a structural feature of the system. In calm periods, overconfidence pushes actors to accumulate massive private debt to bet on existing assets. This dynamic creates speculative bubbles where financial value becomes totally disconnected from the economic reality of territories.

The 2008 subprime crisis remains the most striking example: excessive confidence in American real estate pushed millions of households to go into debt beyond their means, causing a global systemic collapse from which some territories are still suffering the economic and social aftereffects. Today, this same phenomenon of excessive confidence concentrated on a single sector is observed in the AI and semiconductor bubble: stock market valuations reach dizzying heights based on promises of future returns disconnected from physical and energy realities.

When the weight of this debt becomes unsustainable compared to real income (of households, economic actors, or public entities), the system reaches a breaking point, causing a brutal collapse in liquidity. This instability then transforms finance into a generator of uncertainty for the real economy, where global shocks trickle down in cascades to the local scale, undermining territorial actors and ESS structures that depend on stable financing.

2. An extraction of value produced within territories #inequalities

We are witnessing a growing disconnection between where wealth is created (through labor) and where it is captured (through financial remuneration). Financial intermediaries act like suction pumps, capturing value produced locally to concentrate it toward globalized financial centers. This mechanism of capture impoverishes the economic and social fabric of territories because money, instead of circulating in a short circuit to irrigate the real economy, evaporates into opaque intermediation circuits. This value extraction is one of the primary drivers of increasing national and global inequalities.

This disconnection is not only geographical, it is also linked to the scale of our human groupings. Historically, the size of a community (village, medieval city, etc.) imposed natural limits on accumulation. In a system of a few hundred or thousand people, inequalities were structurally limited by physical principles: one could not store more grain than the granaries allowed, nor own more land than human or animal strength could cultivate. Wealth was then intrinsically linked to materiality and the living conditions of the group.

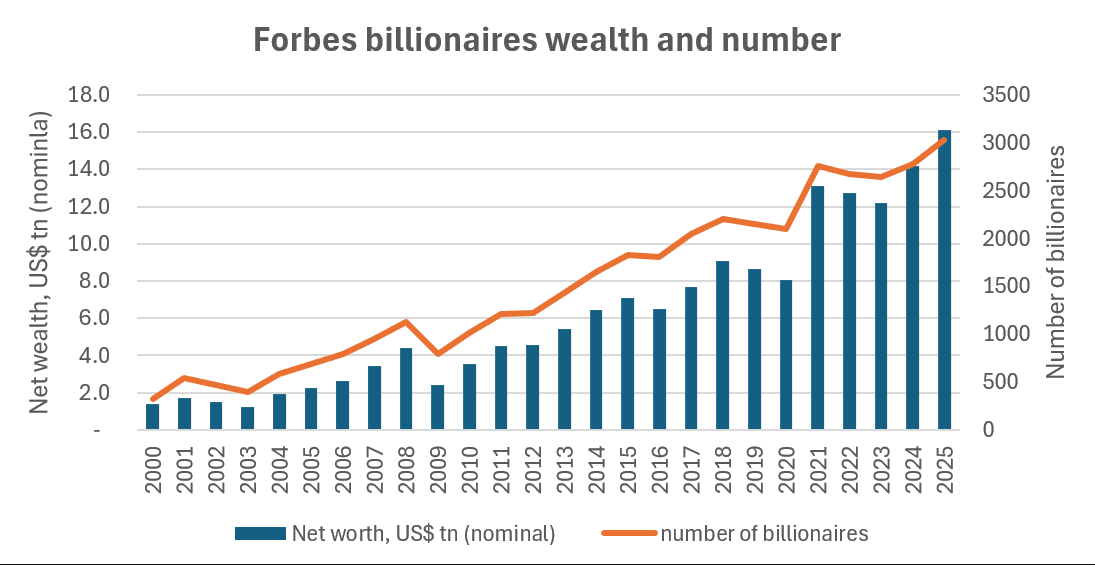

The modern financial system broke this ceiling by dematerializing value. By transforming tangible resources into infinitely divisible and movable digital assets, it allows for limitless accumulation with social regulation systems that are easily bypassed (tax havens, etc.). This phenomenon of siphoning can be observed at the individual scale (the number of billionaires has multiplied by 7 over the last 20 years), the territorial scale, or the international scale (for example, South Africa, which loses nearly one point of GDP every year in remuneration for foreign direct investment).

3. Unsustainable pressure on natural resources #extractivism

The financial system suffers from an endemic ill that Nate Hagens calls "energy blindness." We have built an economic architecture that treats money as the primary source of wealth, whereas it is merely a claim on energy and real resources that we hope to consume in the future. In other words, we have forgotten that behind every transaction, every point of growth, and every dividend, there is a physical transformation of matter and a dissipation of energy (primarily fossil fuels).

This disconnection manifests itself brutally through interest rates. In our current model, the interest rate is a requirement for future growth: to repay a debt with interest, the economy must grow. However, this growth demanded by financial markets is exponential, while the resources of the biosphere are of course, finite.

When interest rates impose a financial return (for example 5% or 7%) higher than the regeneration rate of ecosystems or the increase in energy productivity, finance becomes a force of pure extraction. It forces economic actors to accelerate the consumption rate of natural resources to "feed" the debt. This is the heart of the extractivist mechanism: we burn our natural capital (forests, minerals, biodiversity) to pay the interest on virtual financial capital.

By ignoring thermodynamic limits, the financial nervous system sends price signals that encourage the crossing of regeneration thresholds. This unsustainable pressure transforms finance into an engine of planetary depletion: we are liquidating the physical foundations of our survival to maintain the illusion of growth that continues through time. To escape this blindness, it is imperative to reconnect our financing mechanisms (notably the setting of rates and returns) to the reality of energy flows and the carrying capacity of our territories.

4. An intergenerational Ponzi scheme #injustice

Finally, the current system is characterized by a form of predation upon the future. Monetary creation through debt is a promise made against the labor and resources of future generations. By demanding financial returns that are systematically higher than the biological or physical growth of ecosystems, we are forcing our successors to repay a debt using resources that we will have already largely depleted.

This logic transforms what should be a legacy into a burden. Instead of passing down resilient infrastructure and regenerated environments, we are bequeathing inflated balance sheets and bankrupt natural capital. The financial nervous system, in its current configuration, prioritizes the immediate signal of profit over the transmission of life, acting like a parasite that consumes its host to ensure unsustainable growth.

Pension funds embody the culmination of this temporal predation logic, where we invest our savings today in the hope of future returns that can only be honored by increased siphoning from the real economy of tomorrow. By demanding financial performances disconnected from biological or physical growth, we are creating a system where we literally go into debt to ourselves and following generations. For current and future retirees to receive their pensions, the financial system must extract ever more value from the labor of a shrinking active population (see diagram) and from eroding natural capital.

2/ Toward a relocalization of finance

Faced with this observation, the challenge is not to abolish finance, but to reconnect it to physical (natural resources) and social (communities) markers. If the current global system behaves like a nervous system out of control, it is because it is trapped in an exponential loop disconnected from the signals sent by a finite world. Relocalizing finance is a way to reconnect this nervous system to the physical and human realities of our territories. This evolution must be guided by 4 guiding principles: resilience, proximity, regeneration, and transmission.

Faced with the instability and unpredictability of the globalized system, territorial finance prioritizes resilience. By relying on short-circuit financing mechanisms (a territorial fund acts as the sole intermediary between the capital holder and the borrower) and on long-term investment products, territorial finance helps reduce the impact of global shocks and liquidity crises. No territory can isolate itself from global markets, but the degree of exposure can be reduced. As for the saver, they secure both their capital (which finances local and tangible businesses and infrastructure) and their own lifestyle (food and energy supply chains, territorial preparedness for climate risks, development of trust and solidarity networks, etc.).

Faced with inequality, it fosters proximity. Money is no longer an abstraction evaporating toward financial centers, but a flow that directly irrigates the social and economic fabric of the territory. It then becomes possible to imagine money as a common—a resource managed collectively for the benefit of a community and a region, rather than serving the wealthiest individuals (who possess both the capital and the access to the expertise required to grow it). Instead of placing their savings in distant, opaque pension funds with multiplying intermediaries, citizens, local businesses, and local authorities can deposit their savings into investment products designed and managed by local actors. Beyond the choice of the investment itself, the governance of these territorial funds can also be designed to integrate the voices of savers and residents into the major orientations and strategic decisions of these vehicles.

Faced with the destruction of natural resources, territorial finance prioritizes the regeneration of ecosystems. It would be illusory to think that our society can sustain 8 billion people without drawing from the natural capital at our disposal. Like any species, Homo sapiens has always sought to optimize its resource consumption. All the goodwill in the world will not change this physiological need. However, we do have a degree of control over three elements: (i) the rate at which these resources are consumed; (ii) demographic evolution; and (iii) the capacity of ecosystems to regenerate. On this last point, we must find a way to link the immediate economic cost of regenerative activities to their future economic benefit (or the economic cost of inaction). The insurance sector is the first to be affected (cost of floods, medical care, etc.) and therefore has a central role to play in these reflections.

Faced with the predation of the future, territorial finance bets on transmission. It allows for a shift from a debt-burden logic to an intergenerational investment logic. It ensures that the infrastructure financed today will be an asset for tomorrow's generations, rather than a ransacked house left abandoned the morning after a great party. This approach transforms the figure of the saver into that of a responsible ancestor, capable of projecting common capital beyond their own individual timeframe. By financing tangible assets (forests, green infrastructure, passive housing, energy infrastructure, etc.), territorial finance rehabilitates the notion of common heritage. It no longer settles for seeking an immediate return disconnected from the physical world, but strives to bequeath a healthy and functional world.

In summary, relocalizing finance means giving the economy back its original function: that of taking care of our common home for those who will inhabit it after us (the Greek root of economy: oikos - home - nomos - management).

3/ From idealistic discourse to operational confrontation

Working on the challenges of territorial finance means undertaking a redesign: rebuilding a conscious financial system on a human scale, capable of supporting life instead of consuming it. The intention is laudable and the vision inspiring. However, reality principles quickly come knocking as soon as one attempts to translate this philosophy into a concrete project.

Integrating these principles into an operational financing vehicle requires answering a variety of structural questions:

- The question of temporality: how can we design attractive investment products for patient investors? The current system values immediate liquidity. Here, the goal is to synchronize the timeframe of savings with the long-term cycle of living things (forest growth, thermal renovation, agricultural transition).

- The scale of implementation: a rural living area may lack critical mass, while a region seems too vast to maintain a tangible bond of trust. What intermediate level would allow this local finance to take shape?

- Redefining attractiveness: if yield is no longer the sole compass, what makes an investment desirable? Attractiveness must integrate responses to deeper needs, such as a sense of belonging, conviviality, security (meeting essential needs), pride, and connection to the living world.

- The ancestors' lesson on interest: what returns are reasonable to avoid the runaway effect? The historical distrust of religions (Christianity, Islam, Judaism) toward usury was not just a moral stance, but an intuitive understanding that money cannot grow faster than the physical world without becoming predatory. Reintroducing return caps or loss-sharing logics (inspired by Islamic finance) could be the key to regenerative finance.

Moreover, moving toward action faces structural barriers that must be identified in order to better bypass them:

- The regulatory and fiscal straitjacket: the system is defined by constraints designed for global finance. How can we create financial short circuits without falling under regulations (AMF, prudential) intended for banking giants? A derogation or a regulatory "sandbox" for territorial experimentation will likely be necessary in the long run.

- The battle for skills: setting up such a project requires a rare hybridization of expertise: traditional financial engineering, territorial entrepreneurship, and a keen understanding of ecosystemic challenges. These "five-legged sheep" as we say in French (rare gems) exist, but they still need to be identified.

- Public-private coordination: how can we leverage the complementarity between public grants and private savings without one crowding out the other? The territorial fund must act as a lever, capable of mobilizing private capital where public authorities can no longer act alone.

- The risk of inequalities between territories: a major point of vigilance is the "financial divide." Territories already rich in savings and skills will succeed in their mutation, while declining areas risk being excluded from this relocalization. Solidarity between territorial funds must be designed from the outset.

Furthermore, these reflections on territorial experimentation must not overshadow the need for deeper national and international reforms. We can mention the Chicago Plan of the 1930s (aiming to separate monetary creation from private debt), which remains a source of inspiration for stabilizing the global monetary and financial system (see this revisited proposal by two IMF economists - The Chicago Plan Revisited).

The last structural overhaul of the international monetary system dates back to the Bretton Woods agreements at the end of World War II. History teaches us that such shifts occur almost exclusively following major civilizational shocks. In the current context of the crisis of multilateralism, waiting for a "grand soir" (a revolutionary turning point) in international finance is likely illusory. However, our local initiatives are not disconnected from the global: they act as indispensable micro and meso laboratories to test principles, breathe life into new frameworks of thought, and nourish the imagination necessary for the fundamental reforms that will sooner or later become inevitable.

The coordination of these territorial funds with national projects (such as Opération Milliards, Citizen Capital or the thematic funds of the Banque des Territoires) is, in this respect, essential. The critical challenge is to reverse the usual polarity: national intermediaries must no longer suck local decision-making toward the center, but instead act as reinsurers and multipliers at the service of field initiatives.

At our scale, the upcoming sequence relies on constant iteration:

- Starting from the immediate needs of ESS actors, who are all too often neglected by the traditional banking system;

- Testing the room for maneuver within the current framework;

- Projecting, and translating on the ground, the vision of a finance that ceases to be a blind master and becomes once again a servant of the common good.

This iterative process, as well as the method we deploy to facilitate dialogue between field actors, finance experts, and public decision-makers, is the subject of another notebook. The latter is dedicated to the cooperation engineering required to develop the true capital of tomorrow's finance: trust.

Writting: Igor Louboff

Want to follow the next reports? Subscribe to our newsletter😄